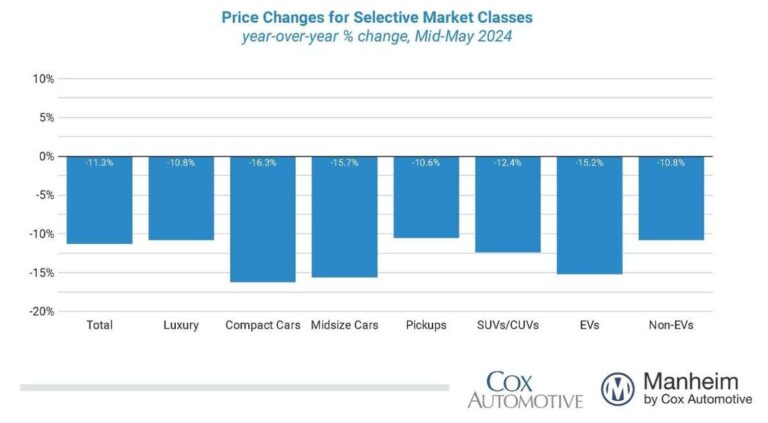

News Arts & Entertainment Hundreds Attend Historic “Counter-Commencement” for Columbia Students in NYC May 17, 2024 Automotive Wholesale Used-Vehicle Prices Increase in First Half of May May 17, 2024 Books & Literature Lit Hub Weekly: May 13 – 17, 2024 May 18, 2024 Building & Construction Van Bergen Kolpa Architecten designs Vertical Farm Beijing as a "beacon in the city" May 18, 2024 Business Ex-Honolulu prosecutor and five others found not guilty in bribery case May 17, 2024 Cryptocurrency This Week in Coins: GameStop Surge Spurs Meme Coin Mania, and Bitcoin Ends on a High May 18, 2024 Education A Beginner’s Guide To Online Teaching Methods May 17, 2024 Family & Parenting What You Can Do to Help Kids in Foster Care May 17, 2024 Fashion & Beauty Procter & Gamble harnesses the power of its brands for the Olympics May 17, 2024 Finance 1 Magnificent Growth Stock Down 12% to Buy and Hold for 5 Years May 18, 2024 Foreign Language 馬來西亞南亞科技原始碼有限公司慶祝網路開發產業卓越15週年 March 11, 2024 Gov & Politics Hakeem Jeffries Calls Justice Alito An Insurrectionist Sympathizer May 17, 2024 Health & Fitness ELD Psychology: Providing Evidence-Based Psychological Treatment in Newcastle and Online May 8, 2024 Home & Garden A Vintage Washstand for a Table in the Living Room May 17, 2024 Lifestyle ‘The Bear’ Season Three Cast Some Very Familiar GQ Faces April 3, 2024 Real Estate New Jersey Court Rules in Support of Independent Contractors in Worker Classification Case May 16, 2024 Religion Celebrating the Anniversary of ‘Dianetics: The Modern Science of Mental Health,’ the All-Time Bestselling Book on the Human Mind May 15, 2024 Science No post found! Sports Central Maine Sports Brings Live Sports Coverage to the Local Community November 8, 2023 Technology Massive Dell data breach hits 49 million users; what this means for your privacy and security May 18, 2024 Travel Tales, trails, and acts of kindness along New Zealand’s 3,000-kilometer Te Araroa trail May 17, 2024

New Jersey Court Rules in Support of Independent Contractors in Worker Classification Case May 16, 2024

Celebrating the Anniversary of ‘Dianetics: The Modern Science of Mental Health,’ the All-Time Bestselling Book on the Human Mind May 15, 2024

Massive Dell data breach hits 49 million users; what this means for your privacy and security May 18, 2024